Setting: Observe a sample \((Y_1,X_1),\dots,(Y_n,X_n)\) with \[ Y_i = X_i\beta+\varepsilon_i=\sum\limits_{j=1}^p \beta_j X_{i,j}+\varepsilon_i\] where \(X_i=(X_{i,1},\dots,X_{i,p})\in\R^{p}\) is a \(p\)-dimensional vector of regressors and \(\beta\) a \(p\)-dimensional vector of regression coefficients.

The vector/matrix \(X_i\) contains the information on individual \(i\) in terms of the \(p\) observable characteristics, e.g., a person’s age, educational background, region/city of residence, etc.

\(\varepsilon_i\) is an error term that emerges naturally due to unobserved characteristics. We assume \(\E\left[\varepsilon_i \vert X_{1i}, ..., X_{pi}\right] = 0.\)

Definition: Regression vs. Classification

Regression:

Regression problems are concerned with estimation of the relationship between a quantitative output \(Y\) and covariates \(X\)

Examples: Wage equations (Mincer equation), estimation of demand functions, ….

Classification

Classification deals with qualitative outcomes \(Y\) (e.g. coded as 0/1, -1/+1).

Examples: Fraud detection (fraud vs. no fraud), image recognition, ….

Concepts: Prediction vs. Inference

Regression methods can be used for two purposes:

1. Prediction

Given an estimated regression model with estimators \(\hat\beta\), what value of \(Y_i\) is to be expected for a person with individual characteristics \(X_i\)? How accurate is the prediction?

2. Inference

What can we say about the relationship of \(Y\) and \(X\)? Does a change in variable \(X_k\)cause an increase/decrease of the outcome variable \(Y\)?

Is the effect meaningful under statistical considerations, i.e., significant?

Is the relationship linear or nonlinear? Is the magnitude of the effect the same for every individual?

Concepts: Prediction vs. Inference

Typically, there is a trade-off between nceaccuracy and interpretability of the model, i.e., often complicated models are associated with good predictive quality but they are hard to interpret.

We will get to know traditional and modern regression methods and see how they compare in terms of predictive quality and interpretability.

Ordinary Least Squares Regression

Prediction

Setting: We want to model the relationship of the dependent variable \(Y\) and the features\(X\).

Our goal is to generate an optimal linear prediction rule for the outcome \(Y\) given the explanatory variables \(X\). We consider \[ X\beta = \sum_{j=1}^{p} \beta_j X_j.\]

It can be shown that, among all linear prediction rules, \(X\beta\) minimizes \[\min_{b \in\R^{p}} \E[(Y-Xb)^2].\]

Ordinary Least Squares Regression

Prediction

Hence, \(X\beta = \E(Y|X)\) is called the best linear prediction rule for \(Y\) given \(X\).

\(X\beta\) is the best linear prediction rule for \(Y\) given \(X\). However, \(X\beta\) is defined in terms of population quantities and, hence, generally not available.

Thus, we use samples, e.g. random draws of \((Y_1,X_1),\dots,(Y_n,X_n)\), to estimate something similar to \(X\beta\), i.e., an optimal prediction rule for \(Y\) given \(X\) that is based on a random sample:

We replace population quantities by sample quantities to obtain an estimate - this is called the “analog principle”.

Ordinary Least Squares Regression

Prediction

Given a random sample, \((Y_1,X_1),\dots,(Y_n,X_n)\), we estimate the coefficients \(\beta\) of the ordinary least squares (OLS) model by minimizing the mean squared error: \[ \min_{b \in\R^{p}} \E_n[(Y-Xb)^2].\]

We obtain the OLS estimates as \[\hat{\beta}=\arg\min\limits_{\beta\in\R^p} \frac{1}{n}\sum\limits_{i=1}^n\big(Y_i-X_i\beta\big)^2=(X^TX)^{-1}X^TY\]

We assume that the \((p \times p)\) matrix \(X^{T}X\) is of full rank and, hence, invertible.

Ordinary Least Squares Regression

Prediction

We know that \(X\beta\) is the best linear prediction rule. What can we say about \(X\hat{\beta}\)? Does it approximate \(X\beta\) well?

It can be shown that \(X\hat{\beta}\) approximates the unknown population regression \(X\beta\) if \(n\) is large as compared to \(p\), i.e., if \(\frac{n}{p} \rightarrow \infty\).

What if the population model is not linear in \(X\)?

Ordinary Least Squares Regression

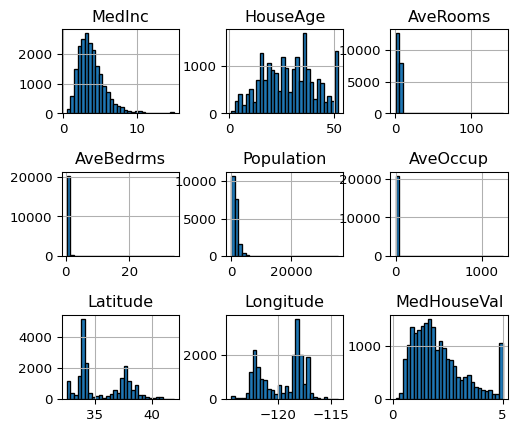

Example: California Housing Data

Code

## Example: Californ Housing Data# Import data from sklearn.datasets import fetch_california_housingimport pandas as pdimport numpy as npcalifornia_housing = fetch_california_housing(as_frame=True)

Description of data set

Code

print(california_housing.DESCR)

Ordinary Least Squares Regression

Example: California Housing Data

Inspect data

Code

california_housing.data.head()

MedInc

HouseAge

AveRooms

AveBedrms

Population

AveOccup

Latitude

Longitude

0

8.3252

41.0

6.984127

1.023810

322.0

2.555556

37.88

-122.23

1

8.3014

21.0

6.238137

0.971880

2401.0

2.109842

37.86

-122.22

2

7.2574

52.0

8.288136

1.073446

496.0

2.802260

37.85

-122.24

3

5.6431

52.0

5.817352

1.073059

558.0

2.547945

37.85

-122.25

4

3.8462

52.0

6.281853

1.081081

565.0

2.181467

37.85

-122.25

Ordinary Least Squares Regression

Example: California Housing Data

Inspect data

Code

california_housing.data.describe()

MedInc

HouseAge

AveRooms

AveBedrms

Population

AveOccup

Latitude

Longitude

count

20640.000000

20640.000000

20640.000000

20640.000000

20640.000000

20640.000000

20640.000000

20640.000000

mean

3.870671

28.639486

5.429000

1.096675

1425.476744

3.070655

35.631861

-119.569704

std

1.899822

12.585558

2.474173

0.473911

1132.462122

10.386050

2.135952

2.003532

min

0.499900

1.000000

0.846154

0.333333

3.000000

0.692308

32.540000

-124.350000

25%

2.563400

18.000000

4.440716

1.006079

787.000000

2.429741

33.930000

-121.800000

50%

3.534800

29.000000

5.229129

1.048780

1166.000000

2.818116

34.260000

-118.490000

75%

4.743250

37.000000

6.052381

1.099526

1725.000000

3.282261

37.710000

-118.010000

max

15.000100

52.000000

141.909091

34.066667

35682.000000

1243.333333

41.950000

-114.310000

Ordinary Least Squares Regression

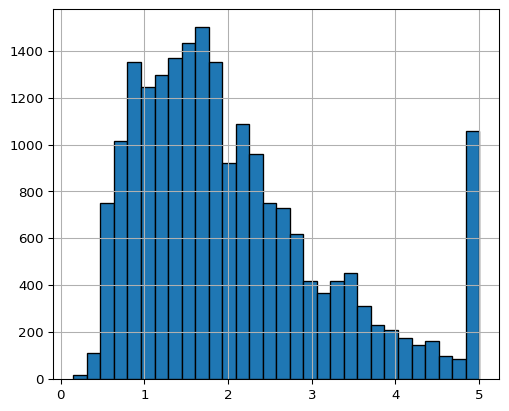

Example: California Housing Data

Inspect the target variable, i.e., the median of the house value for each district

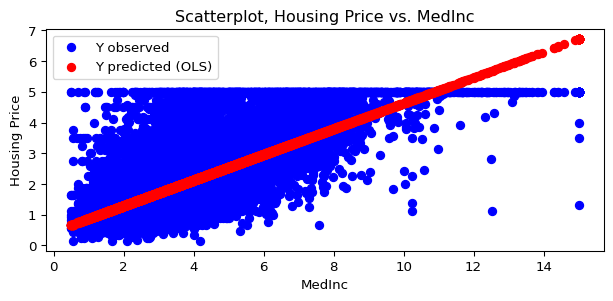

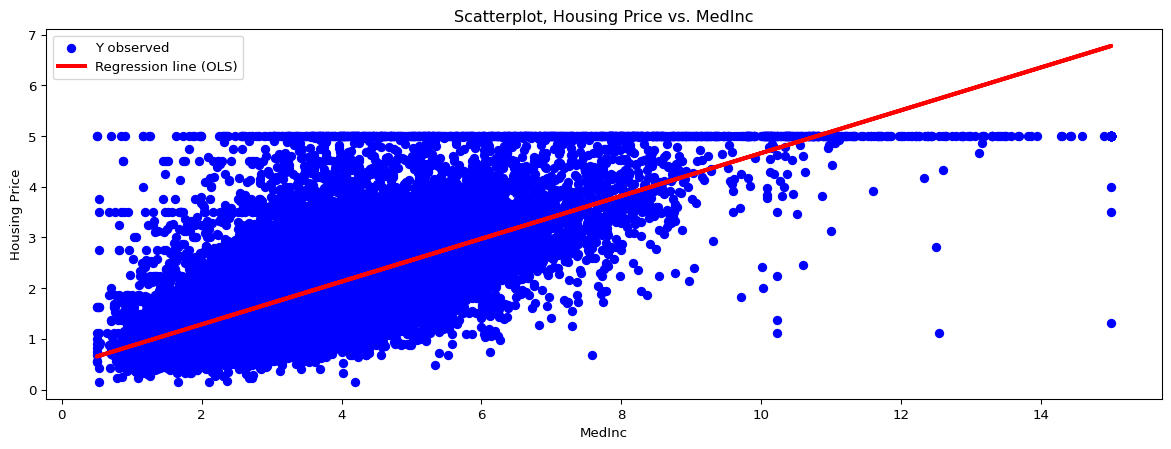

Let us plot the housing prices against the income variable and add the predictions obtained from the regression model.

Code

# We generate predictions from the regression model pred = model.predict(X)plt.figure(1,figsize=(7.5,3))plt.scatter(X, y, color ="blue", label ="Y observed")plt.scatter(X, pred, color ="r", label ="Y predicted (OLS)")plt.xlabel("MedInc")plt.ylabel("Housing Price")plt.title("Scatterplot, Housing Price vs. MedInc")plt.legend()# Let's generate a scatter plot for the simple regression modelplt.show()

Ordinary Least Squares Regression

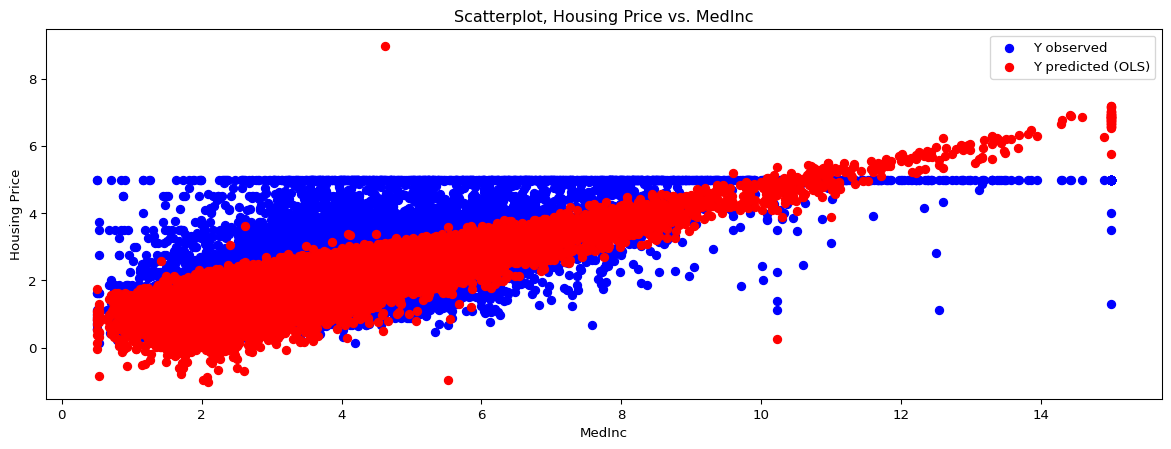

Example 1b - Multivariate Regression

What if we include more covariates in the regression, say all available in the data? How does the coefficient on MedInc change?

Code

X1b = df.to_numpy()model1b = LinearRegression()model1b.fit(X1b, y)# All coefficients: print(np.round(model1b.coef_,4))# And R^2print("R^2: ", np.round(model1b.score(X1b,y),4))

Let us plot the housing prices against the avg. income and add the predictions as obtained from the multivariate regression model (Example 1b).

Code

# We generate predictions from the regression model pred1b = model1b.predict(X1b)plt.figure(1,figsize=(15,5))plt.scatter(df["MedInc"], y, color ="blue", label ="Y observed")plt.scatter(df["MedInc"], pred1b, color ="r", label ="Y predicted (OLS)")plt.xlabel("MedInc")plt.ylabel("Housing Price")plt.title("Scatterplot, Housing Price vs. MedInc")plt.legend()# Let's generate a scatter plot for the multivariate regression modelplt.show()

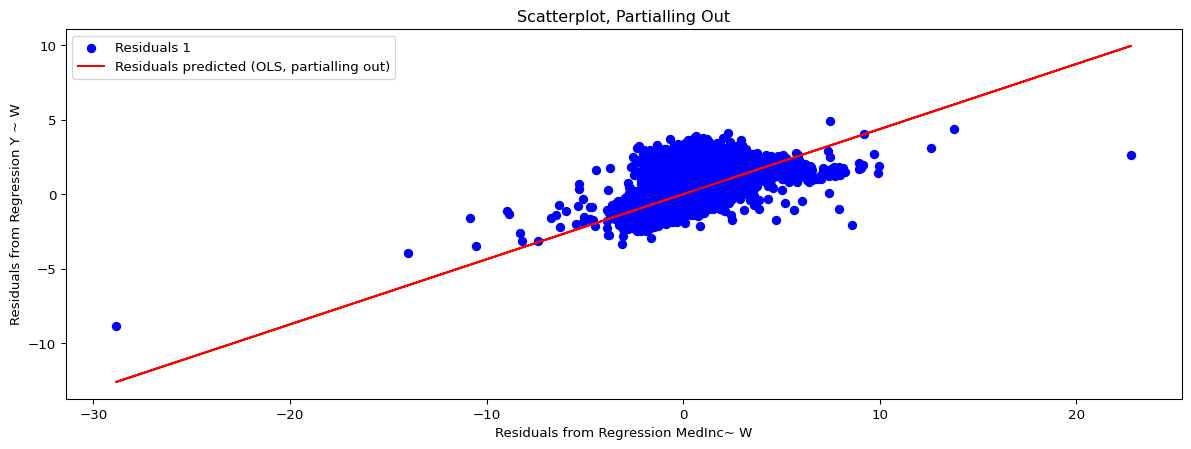

Short Digression: Partialling Out

The linear model does not look as linear as it did in the one-dimensional model. Is there something wrong?

In the multivariate model we have more than one regressor and thus, we do not simply fit a line in a 2-dimensional space to minimize the residuals.

Instead we are now in a higher-dimensional space and try to fit a hyperplane to minimize residuals.

But the linearity can still be recognized using the partialling out result, known as the Frisch-Waugh-Lovell theorem.

Short Digression: Partialling Out

Regress \(Y\) on \(W\), where \(W\) is the matrix with all covariates \(X\)’s except for \(X_j\) (say \(X_{MedInc}\)) and predict the residuals\(r_1\),

Regress \(X_j\) on \(W\) and predict residuals\(r_2\),

Regress \(r_1\) on \(r_2\) and obtain the regression coefficient \(\beta_j\).

As a result, we can create a plot that looks again linear (in the residuals).

Let us now consider how the two models compare in terms of their predictive accuracy using the MSE (Mean Squared Error) in prediction. \[MSE(\hat{y}^{test}_n)=\frac{1}{n^{test}} \cdot \sum_{i=1}^{n^{test}}[(\hat{y}_i^{test}-y_i^{test})^2], \] where we generate predictions for observations i in a test sample \(i = 1,...,n^{test}\), \(n = n^{train} + n^{test}\).

Comparison of Predictive Accuracy of the Models

How we proceed

We split the data randomly into a training (70% of observations) and a test sample (30%),

Estimate the model on the basis of the training sample, and

Assess the predictive accuracy on the basis of the test sample

The ordinary least squares estimator \(\hat{\beta}\) is a consistent estimator for the true regression coefficient \(\beta\) under the assumption stated above.

The estimator is asymptotically normally distributed.

Under homoskedasticity, the OLS estimator is BLUE (Best Linear Unbiased Estimator)

We omit the proofs. But, as you will see in the problem set, you need to understand the results.

Inference

OLS Consistency

Under the assumptions that \(\E[\varepsilon \vert X_1, ..., X_p] = 0\) , \(\rank \E[X'X] = p\) and provided the population regression model is \(Y = X\beta+\varepsilon\), it can be shown that the OLS estimator \(\hat{\beta}\) is a consistent estimator for \(\beta\), i.e., \[\hat{\beta}_n\Pto\beta,\]

as \(n\rightarrow \infty\).

It can also be shown that, under the same assumptions, the OLS estimator is an unbiased estimator for the regression coefficient \(\beta\), i.e.,

Under the following assumptions, there is no linear and unbiased estimator of the \(\beta\) coefficients that has a smaller variance than the OLS estimator \(\hat{\beta}\), i.e., if it holds that

The true regression model is \(Y = X\beta + \varepsilon\),

From the Gauss-Markov Theorem, we can already see that there is an efficiency loss under heteroskedasticity. However, consistency of OLS is not affected by heteroskedasticity.

Inference

Asymptotic Normality of OLS estimator

Consistency and unbiasedness are important properties. However, if we would like to test hypotheses on the model, we need more information on the variability of OLS estimates.

To perform inference, we need to quantify the estimator’s randomness in some way. For instance, we want to test a hypothesis on one of the regression coefficients.

In our California housing data example we could test:

\[H_0: \beta_{MedInc} = 0 ~~ vs. H_1: \beta_{MedInc} \neq 0.\]

Inference

Asymptotic Normality of OLS estimator

If we knew that the estimator \(\hat{\beta}\) was asymptotically normally distributed around the true (unknown) coefficient \(\beta\), we could set up a proper hypothesis test. That is, we could control the probability of a type I error at a significance level \(\alpha\).

Inference

Asymptotic Normality of OLS estimator

We can show that \[\sqrt{n}(\hat{\beta} - \beta) \xrightarrow[]{d} N(0, \Omega),\]

where \(\Omega\) is a variance-covariance matrix with

\[\Omega = (X'X)^{-1}X'\E[\varepsilon \varepsilon'] X (X'X)^{-1}.\]

Inference

Asymptotic Normality of OLS estimator

Under homoskedasticity, for instance as implied by the assumption \(\E\left[\varepsilon \varepsilon' \right] = \sigma^2 I\), \(\Omega\) can be simplified to

Since we know that the OLS estimator is asymptotically normal under appropriate assumptions, we can test the regression coefficients.

Suppose, we are interested in testing whether a regression coefficient \(\beta_j\) (e.g. \(\beta_{MedInc}\)) is different from zero, i.e., our null hypothesis and the alternative are

\[H_0: \beta_{j} = 0 ~~ vs. H_1: \beta_{j} \neq 0.\]

Under the \(H_0\), we now that \(\hat{\beta_j}\) is asymptotically normally distributed around \(\beta_j = 0\).

Tests for OLS

t-test

The probability that the true \(\beta_j\) is zero (\(H_0\)) and that we obtain an estimate \(\hat{\beta}_j\) which is very far away from zero is very small.

It can be shown that, under the \(H_0\), the t-statistic \(t_j\) is \(t\)-distributed with \(n-p-1\) degrees of freedom.

\[t_j = \frac{\hat{\beta}_j - \beta_j}{SE(\hat\beta_j)} \sim t(n-p-1), \] where \(SE(\hat{\beta}_j)\) is the (estimated) standard error of \(\hat{\beta}_j\).

Tests for OLS

t-test

We reject the hypotheses \(H_0\) if \(|t_j| > c_{1-\frac{\alpha}{2}}\) with \(c_{1-\frac{\alpha}{2}}\) being the \((1-\frac{\alpha}{2})\)-quantile of the t-distribution with (n-p-1) degrees of freedom.

Testing one-sided hypotheses is straigthforward.

Tests for OLS

t-test

Questions: Why don’t we have a normal distribution for the test statistic? What if \(n\) is large?

Remember that \(t_j \xrightarrow[]{d}Z \sim\N(0,1)\), i.e., if \(n\) is large enough we can use the \((1-\frac{\alpha}{2})\)-quantiles of the standard normal distribution.

Tests for OLS

Lagrange Multiplier Test

A Lagrange multiplier test allows to test restrictions imposed on the model.

Example: Test whether a subset of \(q\) regression coefficients \(\beta = (\beta_1, ..., \beta_{p-q}, \beta_{p-q+1}, ..., \beta_{p})\) are different from zero.

For the LM test it suffices to regress \(Y\) on the first \(p-q\) regressors and then to regress the residuals of this regression on the \(q\) regressors we are interested in.

The test is based on \(n*R^2\) from the second regression being asymptotically \(\chi^2_q\) distributed.

Tests for OLS

Example continued

What can we say about the hypothesis that \(\beta_{MedInc}\) is different from zero?

\[H_0: \beta_{MedInc} = 0 ~~ vs. H_1: \beta_{MedInc} \neq 0\]

Unfortunately, the sklearn package does not provide tests as it is mainly developed for predictions ➡️ Package statsmodel

Tests for OLS

Example continued

Let’s estimate the model from the previous example

Code

import statsmodels.api as sm# First, we add an intercept to the dataXc = sm.add_constant(X)ols = sm.OLS(y,Xc)ols = ols.fit(cov_type ="HC3")ols.summary()

OLS Regression Results

Dep. Variable:

y

R-squared:

0.473

Model:

OLS

Adj. R-squared:

0.473

Method:

Least Squares

F-statistic:

1.394e+04

Date:

Thu, 02 Jul 2026

Prob (F-statistic):

0.00

Time:

13:11:22

Log-Likelihood:

-25623.

No. Observations:

20640

AIC:

5.125e+04

Df Residuals:

20638

BIC:

5.127e+04

Df Model:

1

Covariance Type:

HC3

coef

std err

z

P>|z|

[0.025

0.975]

const

0.4509

0.014

32.021

0.000

0.423

0.478

x1

0.4179

0.004

118.060

0.000

0.411

0.425

Omnibus:

4245.795

Durbin-Watson:

0.655

Prob(Omnibus):

0.000

Jarque-Bera (JB):

9273.446

Skew:

1.191

Prob(JB):

0.00

Kurtosis:

5.260

Cond. No.

10.2

Notes: [1] Standard Errors are heteroscedasticity robust (HC3)

Tests for OLS

Example continued

We can print the confidence intervals using our OLS estimation results.

Code

ols.conf_int(alpha=0.05)[1,:]

array([0.41100013, 0.42487685])

The predictions can also be plotted in statsmodel

You can verify yourself that the predictions are identical to those obtained with sklearn

Quantile Regression

Motivation

Remember, what does OLS actually do?

“What the regression curve does is give a grand summary for the averages of the distributions corresponding to the set of xs. We could go further and compute several different regression curves corresponding to the various percentage points of the distributions and thus get a more complete picture of the set. Ordinarily this is not done, and so regression often gives a rather incomplete picture. Just as the mean gives an incomplete picture of a single distribution, so the regression curve gives a correspondingly incomplete picture for a set of distributions” (Mosteller and Tukey 1977)

Quantile Regression

Motivation

Remember, what does OLS actually do?

“[…] quantile regression results offer a much richer, more focused view of the applications than could be achieved by looking exclusively at conditional mean models.” (Koenker 2005, 38:25)

Main reference for quantile regression: Koenker (2005)

Quantile Regression

Recap: What is a quantile?

Unconditional quantile:

\(F_{Y_i}(y)\) is the cdf of \(Y_i\). Then \(q_{Y_i}(\tau)\) is the \(\tau\) quantile of \(Y_i\) as it solves

Alternatively, we can write \[F(q_{Y_i}(\tau)) = \tau.\]

Quantile Regression

Recap: What is a quantile?

Generally, we are interested in conditional quantiles, i.e., the quantile of \(Y_i\) given values of \(X_i\).

\(F_{Y_i|X_i}(y)\) is the conditional cdf of \(Y_i\) given \(X_i\) and, thus, \(q_{Y_i|X_i}(\tau)\) is the conditional \(\tau\)-quantile of \(Y\) as it is the solution to

\[F(q_{Y_i|X_i}(\tau)|X_i) = \tau.\]

Major Question: How do covariates affect quantiles of the outcome variable?

Quantile Regression

Recap: What is a quantile?

We are still in the linear model set up, i.e., we model our outcome as

\[Y_i = X_i\beta + \varepsilon_i,\] where we assume that \(\varepsilon\) is i.i.d. and independent of \(X\).

The conditional quantile function of \(Y\) is then:

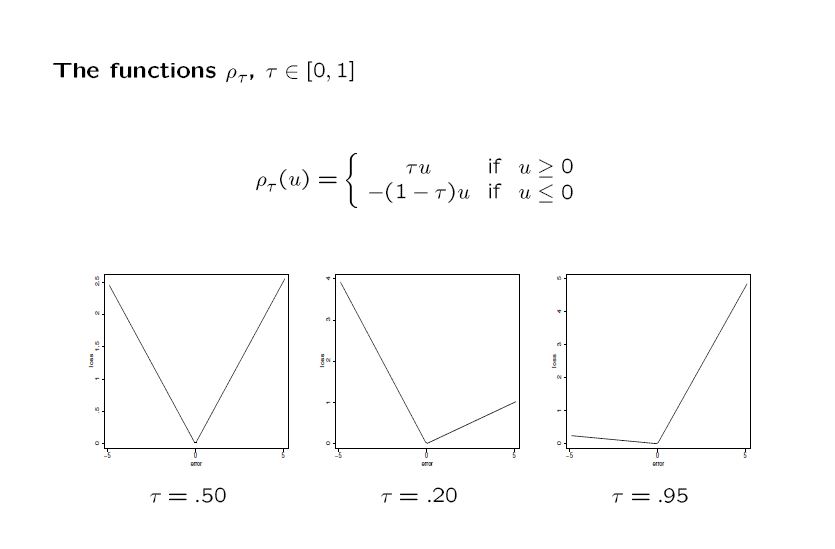

with \(\rho_\tau = (\tau I[\varepsilon \ge 0] + (1-\tau)I[\varepsilon<0])|\varepsilon| = (\tau - I[\varepsilon<0])\varepsilon\). \(I(\cdot)\) is an indicator function assuming value one if statement \(\cdot\) is true.

We skip the details on the optimization problem. Details can be found in the textbook of Koenker (2005)

Quantile Regression

Illustration of Check Function

(taken from Bonhomme, 2008)

Quantile Regression

Median Regression = LAD Regression

The median is a special case of a quantile (i.e., the 0.5-quantile). For the median regression model, we have \(\tau = \frac{1}{2}\) and

Hence, the median estimator minimizes the absolute deviations from the \(Y\) values whereas the conditional mean estimator (OLS) is the minimizer of the squared error. The median estimator is therefore called LAD-estimator (Least Absolute Deviations).

Quantile Regression

Computation / Solving the Minimization Problem

Quantile regression estimators are not as nice to compute as the OLS estimator because the objective function is non-differentiable (how would you set up the FOC?).

However, the minimization problem can be reformulated as a linear program which can be solved. We omit the computational details. They can be found in Koenker (2005) or (less technical) in Bonhomme (2008).

Efficient optimization methods have been developed and implemented.

Quantile Regression

Interpretation of Coefficients

In the OLS model we have that \[E(Y|X) = X\beta \]

leading us to the interpretation of \(\beta\) as a partial derivative \[\frac{\partial E(Y|X)}{\partial X_j} = \beta_j.\]

In the quantile regression we have \(q_{Y|X}(\tau) = X\beta_\tau\) and thus \[\frac{\partial q_{Y|X}(\tau)}{\partial X_j} = \beta_\tau .

\]

Asymptotics for Quantile Regression

Consistency

As \(\beta_\tau\) minimizes \(\E[\rho_\tau [Y-X\beta]]\), it can be shown that \(\hat{\beta}_\tau\) is a consistent estimator for \(\beta\) (a quantile estimator is a \(M\)-estimator which can easily be observed in the case of median regression).

Asymptotics for Quantile Regression

Asympotic Normality

Moreover, Koenker (2005) shows that \(\hat{\beta_\tau}\) is asymptotically normally distributed under appropriate assumptions. However the proof of asymptotic normality is complicated by the lack of differentiability of the objective function.

Asymptotics for Quantile Regression

Inference

Since we know that the \(\hat{\beta}_\tau\) is asymptotically normal, we can test hypotheses and construct confidence intervals. To do this we can either estimate standard errors by their analytical expressions (Hendricks-Koencker, 1991 and Powell, 1991) or to use a bootstrap procedure. We can use tests that are similar to those for the OLS model.

Attractive Properties of Quantile Regression

The quantile regression model shares nice properties:

Robustness to outliers: As you remember from the basic statistics course, the median is robust to outliers (in contrast to the mean). This nice property translates into the quantile regression framework.

Equivariance to monotone transformations: Suppose there is a monotone transformation \(h()\) which is imposed on the outcome variable. Then the quantile estimates remain unchanged, i.e.,

\[q_{h(Y_i)|X_i}(\tau) = h(q_{Y_i|X_i} (\tau)).\]

This property does not hold for the conditional mean if \(h()\) is non-linear.

Attractive Properties of Quantile Regression

Example: Wages and log-Wages

In labor economics, a frequent task is to estimate wage equations. The wages are denoted as \(Y_i^*\). However, typically a log-linear wage regression is estimated, i.e. \(Y_i = \ln(Y_i^*)\) is used as a dependent variable.

In contrast, the conditional mean does not share this equivariance property.

How does the meaning of the OLS and quantile regression coefficients change if \(y_i\) is subject to a monotone transformation \(h(\cdot)\)?

Quantile Regression

California Housing data

Code

pred = model.predict(X)plt.figure(1,figsize=(15,5))plt.scatter(X, y, color ="blue", label ="Y observed")plt.plot(X, pred, color ="r", linewidth =3, label ="Regression line (OLS)")plt.xlabel("MedInc")plt.ylabel("Housing Price")plt.title("Scatterplot, Housing Price vs. MedInc")plt.legend()plt.show()

Quantile Regression

California Housing data

Code

from statsmodels.regression.quantile_regression import QuantRegqr = sm.QuantReg(y,Xc)med = qr.fit(q =0.5)med.summary()

QuantReg Regression Results

Dep. Variable:

y

Pseudo R-squared:

0.3107

Model:

QuantReg

Bandwidth:

0.1220

Method:

Least Squares

Sparsity:

1.695

Date:

Thu, 02 Jul 2026

No. Observations:

20640

Time:

13:11:22

Df Residuals:

20638

Df Model:

1

coef

std err

t

P>|t|

[0.025

0.975]

const

0.2058

0.013

15.371

0.000

0.180

0.232

x1

0.4387

0.003

141.268

0.000

0.433

0.445

Quantile Regression

California Housing data

Code

med = qr.fit(q =0.5)q005 = qr.fit(q =0.05)q01 = qr.fit(q =0.1)q02 = qr.fit(q =0.2)q08 = qr.fit(q =0.8)q09 = qr.fit(q =0.9)q095 = qr.fit(q =0.95)predmed = med.predict(Xc)pred005 = q005.predict(Xc)pred01 = q01.predict(Xc)pred02 = q02.predict(Xc)pred08 = q08.predict(Xc)pred09 = q09.predict(Xc)pred095 = q095.predict(Xc)p_quant = plt.figure(1,figsize=(15,5))plt.scatter(X, y, color ="blue", label ="Y observed")plt.plot(X, pred, color ="r", linewidth =3, label ="Regression line (OLS)")plt.plot(X, predmed, color ="g", linewidth =3, label ="Regression line (Median)")plt.plot(X, pred005, color ="g", linewidth =1)plt.plot(X, pred01, color ="g", linewidth =1)plt.plot(X, pred02, color ="g", linewidth =1)plt.plot(X, pred08, color ="g", linewidth =1)plt.plot(X, pred09, color ="g", linewidth =1)plt.plot(X, pred095, color ="g", linewidth =1)plt.xlabel("MedInc")plt.ylabel("Housing Price")plt.title("Scatterplot, Housing Price vs. MedInc, Median Regression")plt.legend()p_quant.show()

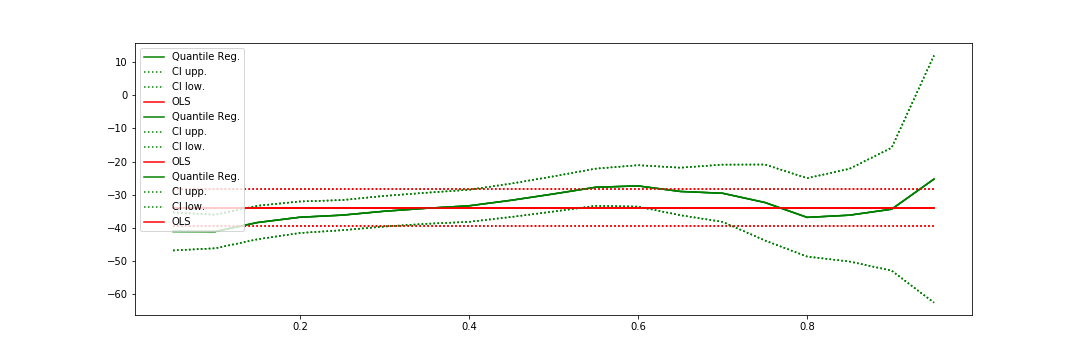

Quantile Regression

California Housing data

We can also plot the regression coefficients obtained from quantile regression for various quantiles \(\tau \in (0,1)\).

Quantile Regressionit

California Housing data: Censoring

Suppose, the dependent variable of the Boston housing data is censored at a value of 15. What happens to the regression coefficients of OLS and median regression?

Question: If quantile regression is so attractive, why is OLS regression so popular?

ML-Methods

So far, we have talked about ordinary least squares regression.

“Machine Learning” methods have been developed, in particular to generate precise predictions in situations with many covariates \(X\), i.e., \(p > n\).

Remember the (OLS) regression setting: We observe a sample \((Y_1,X_1),\dots,(Y_n,X_n)\) with \[ Y_i = X_i\beta+\varepsilon_i=\sum\limits_{j=1}^p \beta_j X_{i,j}+\varepsilon_i\] where \(X_i=(X_{i,1},\dots,X_{i,p})\in\R^{p}\) is a \(p\)-dimensional vector of regressors.

Problem: What happens if \(p>n\)?

ML-Methods

Problem: What happens if \(p>n\)?

\[n\ge\rank(X)=\rank(X^TX)\in \R^{p\times p}\] Therefore \((X^TX)\) does not have full rank and is not invertible.

How can \(p>n\) occur?

Rich data sets: New data sets collect a lot of information on individuals, e.g. imagine a large online shop collecting data on past purchases

New data types: Unstructured data such as text or images are typically stored in high-dimensional data structures

Constructed regressors: The relationship of \(Y\) and \(X\) might be non-linear and the \(X\) are transformed

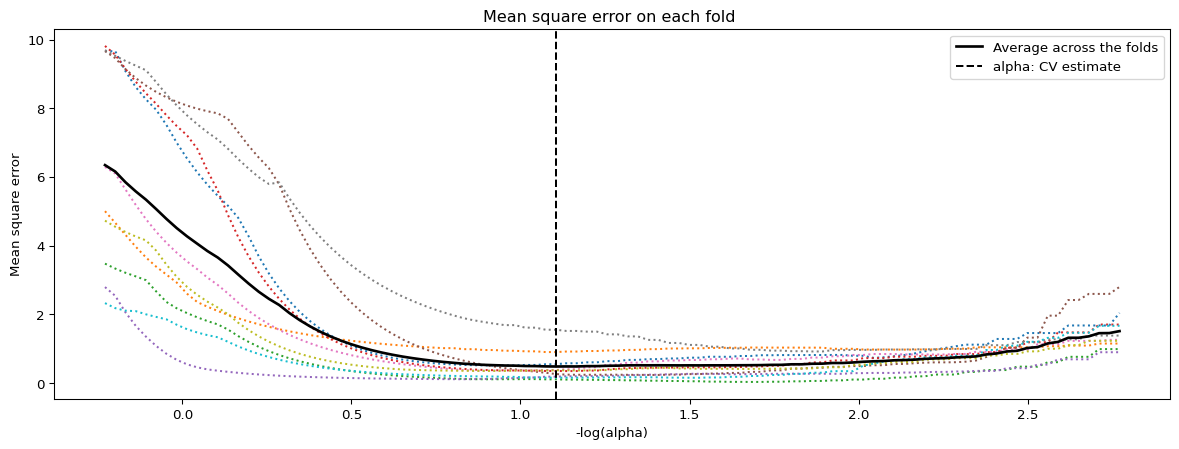

Choice of \(\lambda\): \(K\)-fold Cross Validation

\(K\)-fold cross validation to select \(\lambda\) proceeds as

Split the data randomly into \(K\) “folds” of equal size.

Given a fold \(k = 1,..., K\), we use the \(k-1\) folds as a training set. We train the model by varying \(\lambda\). The fold \(k\) is used as a testing set. For each \(k\), we obtain a \(MSE_k(\lambda)\).

We get a \[MSE_{CV}(\lambda)=\frac{1}{K}\sum_{k=1}^{K} MSE_k(\lambda)\]

We choose the \(\lambda\) that minimizes \(MSE_{CV}\).

Lasso

Code

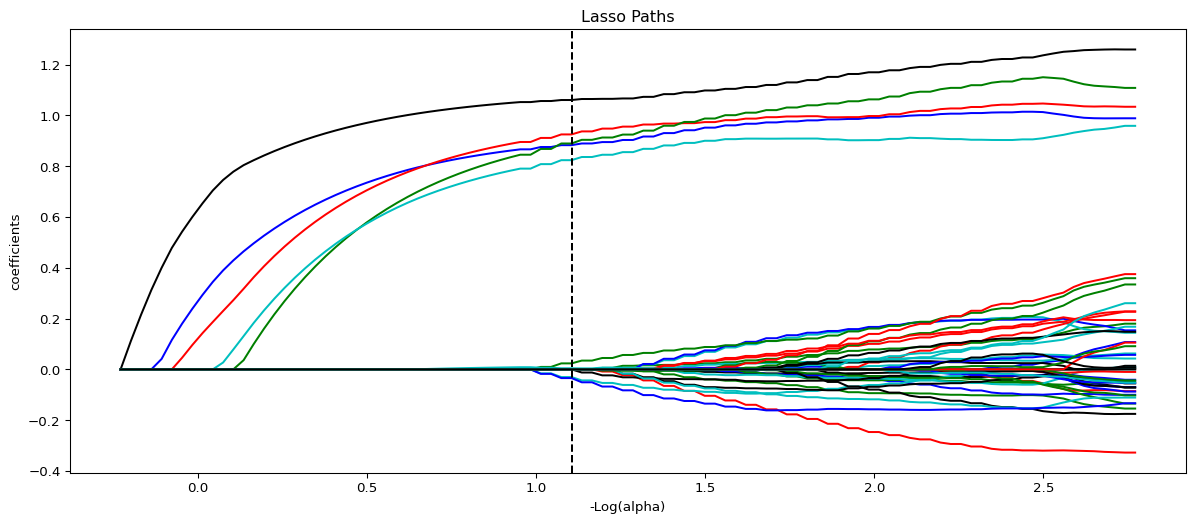

from sklearn import linear_modellassocv_reg = linear_model.LassoCV(cv=10,fit_intercept =False)model = lassocv_reg.fit(X, Y)# Display resultsm_log_alphas =-np.log10(model.alphas_)plt.figure(1,figsize=(15,5))plt.plot(m_log_alphas, model.mse_path_, ':')plt.plot(m_log_alphas, model.mse_path_.mean(axis=-1), 'k', label='Average across the folds', linewidth=2)plt.axvline(-np.log10(model.alpha_), linestyle='--', color='k', label='alpha: CV estimate')plt.legend()plt.xlabel('-log(alpha)')plt.ylabel('Mean square error')plt.title('Mean square error on each fold ')# '(train time: %.2fs)' )#% t_lasso_cv)plt.axis('tight')plt.show()

Y2_est = model.predict(X2) # Prediction for Y2MSE = np.mean((Y2-Y2_est)**2)print("Mean-Squared-Error:",MSE)

Mean-Squared-Error: 0.27389197732839965

OLS

What would OLS look like in this setting?

Code

Y_ols_est = ols.predict(X) # Prediction for YMSEins = np.mean((Y-Y_ols_est)**2)print("Mean-Squared-Error (INS):",MSEins)

Mean-Squared-Error (INS): 3.30616073535597e-29

Code

Y2_ols_est = ols.predict(X2) # Prediction for Y2MSE = np.mean((Y2-Y2_ols_est)**2)print("Mean-Squared-Error (OOS):",MSE)

Mean-Squared-Error (OOS): 11.114031890411887

Lasso

Intuition: What does Lasso actually do?

Lasso imposes the (approximate) sparsity assumption on the coefficients \(\hat{\beta}\).

This leads to both coefficient shrinkage and variable selection.

Shrinkage: All coefficents are shrunk towards zero, without sacrificing too much fit.

Variable Selection: Shrinkage ends up with setting many coefficents exactly zero, i.e., the associated variables do not have any impact on the prediction of \(Y\) anymore.

It can be shown that, under the (approximate) sparsity assumption, Lasso approximates \(X\beta\) well, i.e., without overfitting the data.

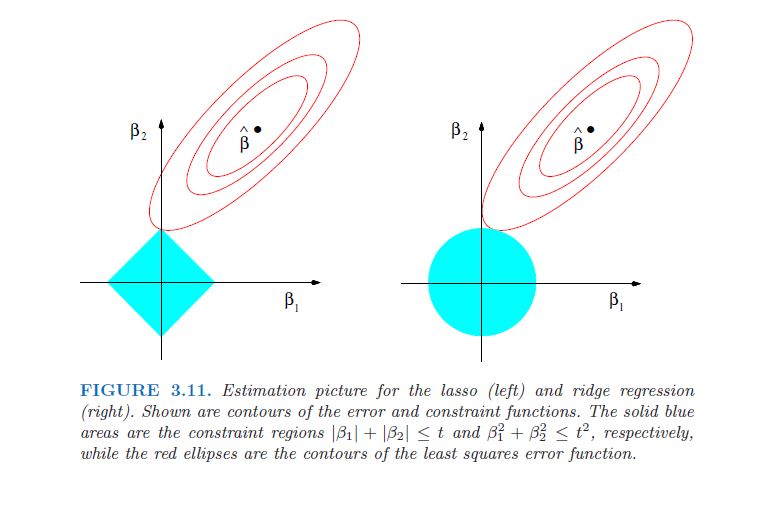

Lasso performs penalized regression with a \(l_1\)-penalty. Alternatively, one could use the \(l_2\)-norm of the estimators. This gives rise to Ridge.

Define \[\begin{align*}\hat{\beta}^{Ridge}:&=\arg\min\limits_{\beta\in\R^p} \frac{1}{n}\sum\limits_{i=1}^n\big(Y_i-X_i\beta\big)^2+\lambda\sum\limits_{j=1}^p\beta_j^2\\

&=\arg\min\limits_{\beta\in\R^p} \E_n\left[\big(Y_i-X_i\beta\big)^2\right]+\lambda\|\beta_j\|_2^2\end{align*}\] where \(\lambda>0\) is a tuning parameter, typically chosen by cross-validation.

Ridge

Ridge shrinks coefficients more agressively and more “democratically” towards zero.

Large values of \(\beta\) are penalized more and small values are penalized less severely than by the Lasso.

\(\Rightarrow\) Ridge only performs shrinkage, no selection.

Ridge performs well in “dense” models, i.e., the \(\beta\) are small but not zero.

Elastic Net is a combination of Lasso and Ridge as it incorporates both a \(l_1\) and \(l_2\) penalty. \[

\begin{align*}\hat{\beta}^{ENet}:&=\arg\min\limits_{\beta\in\R^p} \frac{1}{n}\sum\limits_{i=1}^n\big(Y_i-X_i\beta\big)^2+ \lambda_1\sum\limits_{j=1}^p\big| \beta_j\big| + \lambda_2\sum\limits_{j=1}^p\beta_j^2

\end{align*}

\]

Elastic net performs shrinkage on large coefficients as agressively as Ridge and on small coefficients as agressively as Lasso.

As long as \(\lambda_1 > 0\), elastic net performs variable selection.

Koenker, Roger. 2005. Quantile Regression. Vol. 38. Cambridge university press.

Mosteller, Frederick, and John W Tukey. 1977. “Data Analysis and Regression. A Second Course in Statistics.”Addison-Wesley Series in Behavioral Science: Quantitative Methods.